Content

The types of accounts to which this rule applies are expenses, assets, and dividends. As noted earlier, expenses are almost always debited, so we debit Wages Expense, increasing its account balance. Since your company did not yet pay its employees, the Cash account is not credited, instead, the credit is recorded in the liability account Wages Payable. This standard discusses fundamental concepts as they relate to recordkeeping for accounting and how transactions are recorded internally within Indiana University. Information presented below walks through specific accounting terminology, debit and credit, as well as what are considered normal balances for IU. A dangling debit is a debit balance with no offsetting credit balance that would allow it to be written off.

A business might issue a debit note in response to a received credit note. Mistakes (often interest charges and fees) in a sales, purchase, or loan invoice might prompt a firm to issue a debit note to help correct the error. For example, if Barnes & Noble sold $20,000 worth of books, it would debit its cash account $20,000 and credit its books or inventory account $20,000. This double-entry system shows that the company now has $20,000 more in cash and a corresponding $20,000 less in books. Moreover, Nanonets is backed by machine learning, so it gets smarter with every invoice it processes.

What is the normal balance?

Understanding the basics of a normal balance in the Chart of Accounts is crucial for effective procurement. By creating a clear and consistent system for recording financial transactions, businesses can improve their accuracy in tracking expenses and making informed purchasing decisions. The Chart of Accounts is an essential component in any financial system because it allows businesses to accurately record their financial transactions.

Let’s use what we’ve learned about debits and credits to determine what this accounting transaction is recording. The first step is to determine the type of accounts being adjusted and whether they have a debit or credit normal balance. The side that increases (debit or credit) is referred to as an account’s normal balance.

Recording Credits And Debits For Owner’s Equity Accounts

In a general ledger, or any other accounting journal, one always sees columns marked “debit” and “credit.” The debit column is always to the left of the credit column. Under this column, the difference between the debit and the credit is recorded. If the debit is larger than the credit, the resultant difference is a debit, and this is listed as a numerical figure. Thus, if the entry under the balance column is 1,200, this reflects a debit balance.

- Harold Averkamp (CPA, MBA) has worked as a university accounting instructor, accountant, and consultant for more than 25 years.

- Book this 30-min live demo to make this the last time that you’ll ever have to manually key in data from invoices or receipts into ERP software.

- To better understand AP, we must first know the basic concept of debits and credits.

- He most recently spent two years as the accountant at a commercial roofing company utilizing QuickBooks Desktop to compile financials, job cost, and run payroll.

- To show how the debit and credit process works within IU’s general ledger, the following image was pulled from the IUIE database.

The Normal Balance or normal way that a liability, equity, or revenue is increased is with a credit (negative amount). These are crucial elements in procurement that can help streamline your financial processes. By understanding what the Chart of Accounts is and how to create a Normal Balance within it, you’ll be able to better manage your finances and make informed decisions for your business. Normal balance of an account refers to the ledger side where the balance of an account is normally seen or expected. In simple words, it means whether a particular account has a debit balance or a credit balance. Below is a basic example of a debit and credit journal entry within a general ledger.

Record an Expense Purchased on Vendor Credit

A debit is an accounting entry that creates a decrease in liabilities or an increase in assets. In double-entry bookkeeping, all debits are made on the left side of the ledger and must be offset with corresponding credits https://www.bookstime.com/ on the right side of the ledger. On a balance sheet, positive values for assets and expenses are debited, and negative balances are credited. When a company earns money, it records revenue, which increases owners’ equity.

If a transaction didn’t balance, then the balance sheet would no longer balance, and that’s a big problem. Temporary accounts (or nominal accounts) include all of the revenue accounts, expense accounts, the owner’s drawing account, and the income summary account. Generally speaking, the balances in temporary https://www.bookstime.com/articles/normal-balance accounts increase throughout the accounting year. At the end of the accounting year the balances will be transferred to the owner’s capital account or to a corporation’s retained earnings account. Within IU’s KFS, debits and credits can sometimes be referred to as “to” and “from” accounts.

AccountingTools

A double-entry accounting system records each transaction as a debit and a credit. For example, a company’s checking account (an asset) has a credit balance if the account is overdrawn. Sometimes a debit will increase an account and sometimes it will decrease an account. To effectively use double-entry accounting, it is critical that you understand how debits and credits work. However, in double-entry accounting, these terms are used differently than you may be used to.

- The account payable is a liability account used to track the amount of money a company owes to its vendors or other outside parties.

- As such, in a cash account, any debit will increase the cash account balance, hence its normal balance is a debit one.

- For asset and expense accounts, the normal balance is a debit balance.

- These accounts, like debits and credits, increase and decrease revenue, expense, asset, liability, and net asset accounts.

- To create a Normal Balance, start by identifying each account in the Chart of Accounts and determining its classification – asset, liability, equity, revenue or expense.

Whenever cash is received, the asset account Cash is debited and another account will need to be credited. Since the service was performed at the same time as the cash was received, the revenue account Service Revenues is credited, thus increasing its account balance. After the business has settled its debt to the vendor, it is required to lessen the responsibility connected to the debt.

Terminology of Accounting

This situation could possibly occur with an overpayment to a supplier or an error in recording. Once you determine each account’s normal balance direction (debit or credit), finalize your chart by listing them under their respective categories with their designated balances indicated. With this information at hand, it becomes easier to make informed decisions regarding purchases and payments that align with the organization’s financial goals. Creating a Normal Balance in the Chart of Accounts is crucial for effective procurement management. Let’s say there were a credit of $4,000 and a debit of $6,000 in the Accounts Payable account. However, the difference between the two figures in this case would be a debit balance of $2,000, which is an abnormal balance.

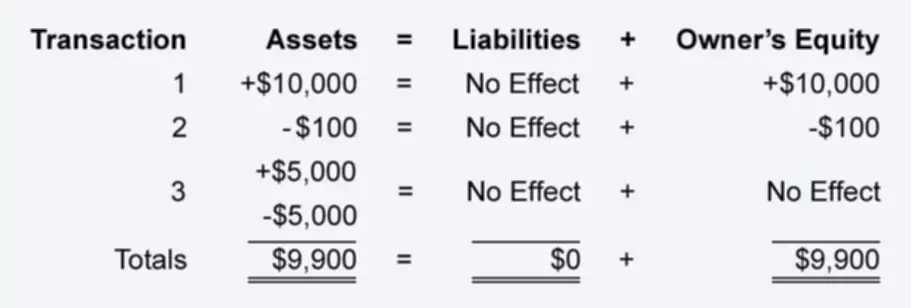

It’s essentially a list of all the accounts used to track income, expenses, assets, liabilities, and equity. Each account has a unique code assigned to it for easy identification and tracking. The types of accounts lying on the left side of these equations carry a debit balance while those on the right-side carry a credit balance. We can illustrate each account type and its corresponding debit and credit effects in the form of an expanded accounting equation.

Leave a Comment